- English

- Hindi

- Tamil

CUSTOMER PROTECTION / GRIEVANCE POLICY

(Approved by the Board on March 27, 2026)

Introduction:

LivQuik Technology (India) Private Limited (“the Company” or “LivQuik” or ‘LQ”) is a ‘Company’ incorporated under ‘Companies Act, 1956’ with its registered office in Chennai. The Company is authorized by the Reserve Bank of India (“RBI”) to issue Prepaid Payment Instruments (“PPI”) under the RBI’s Master Directions on PPIs (“PPI Master Directions”). The PPI Master Directions mandate the Company to formulate and disclose a Board approved ‘Customer Grievance Redressal policy’ to protect the rights of the customer. Additionally, the PPI Master Directions and applicable Guidelines require the Company to appoint a Nodal Grievance Redressal Officer and institute sections on reporting of unauthorized PPI transactions & defining the extent of customer’s liability.

LivQuik’s PPI product revolves around issuance of digital wallets, being offered under the brand name - ‘LivQuik’. The wallet provides an alternative to cash-based transactions and is used widely across various segments of the society. The Company places immense emphasis on ensuring first time resolution and building customer trust and confidence. Further, LivQuik undertakes regular trainings for its employees to ensure that consumer’s queries and grievances are handled in an appropriate manner.

In view of the above, the Company has framed a consolidated Grievance Redressal Policy (“the Policy”) with the approval of its Board of Directors (“Board”) for its PPI based products and services. The Company has made this policy accessible to all the Users on its mobile app, its products and website.

Key Definitions:

For the purpose of the Policy, some key definitions are as follows:

- “Customer” or “Complainant” or “User” – is an individual or an entity who is an end-user of the PPI wallet-based products and services offered by the Company;

- “Grievance” or “Complaint” - refers to any correspondence that is comprehensive and explicit in nature that conveys a gap in the promised and delivered service levels which may be technical or communicative errors. This includes the incidence of a Customer reporting cases of loss or theft of card or authentication data or if any fraud / abuse and any ‘unauthorised transaction’. Additionally, Grievance or Complaints can be lodged against inappropriate conduct, acts of omission or commission, however, any feedbacks/explanations will not be considered as Grievances or Complaints;

- “Nodal Officer” - refers to the Officer appointed by the Company to manage Customer Grievances/Complaints and ensure their redressal in accordance with the prescribed process, Turn-Around-Time (TAT) and the escalation matrix.

- “Product” or “LivQuik” or “Wallet” or “Card” refers to the PPI wallet called ‘LivQuik’ offered by the Company.

- “Unauthorised transaction” - refers to transactions where the amount is debited to the Customer’s account without Customer’s consent.

Objective:

The Objectives of this Policy are to:

- Formulate a robust Grievance Redressal mechanism to be implemented for all Products offered by the Company;

- Provide a 24x7 multi-channel complaint registering facility for the Customer;

- Reiterate that Customer is the prime focus of all initiatives and strategies developed by the Company and it places immense importance on ensuring customer protection;

- Provide its Customers with a transparent experience by providing the Customer with details on ‘Turn-Around-Time’ (TAT), Escalation matrix, Customer liability on account of Unauthorised transactions and the Nodal Officer;

- Ensure that all Grievances / Complaints are resolved in a seamless, efficient and effective manner, to the satisfaction of the Customer and within the defined timelines;

- Provide its Customers with transparent communication regarding their Grievance process and the ability to track their complaints;

- Disclose all the details regarding the Company’s Grievance Redressal mechanism in the public domain in an effort to promote transparency;

- Ensure that LivQuik, its employees and its personnel work in good faith and without prejudice, in the interests of the Company’s Users;

- Treat all Customers fairly and equally at all times;

- Enhance the Company’s products and services developed based on regular Customer feedback to address customer grievances.

Team sensitization on handling complaints:

The Company ensures that its personnel responsible for Customer service at all levels undergo regular trainings to ensure that consumer’s queries and grievances are handled in an appropriate manner, to the satisfaction of the Customer.

Consent includes authorization of a transaction debit either through additional authentication required by LivQuik such as use of security passwords, input of dynamic password (OTP) or any other electronic authentication option provided by LivQuik.

The Company encourages its personnel to work in a manner which allows the Company to offer a first-time resolution and in turn build the consumer trust and confidence. This reflects in both the Company’s operations as well as the Customer communications.

Grievance Redressal Mechanism:

The Company values all its customers and assures a sincere and transparent approach in redressing their grievances. In an effort to provide its customers with satisfactory grievance redressal, LivQuik has formulated a comprehensive grievance redressal mechanism. The Company has designed the mechanism to ensure that its customers can seamlessly register their complaints via a multi-channel set-up. Additionally, the mechanism has a 4-step escalation matrix to ensure that a Customer is provided with adequate appeals. The Company has also instituted TATs within the mechanism at different stages to ensure time-bound redressal of complaint.

Escalation Matrix and TAT

Grievance Redressal process

A Customer can register a complaint via either of the two channels provided by the Company. The channels are as under

| Sr.No | Channel | Details |

|---|---|---|

| 1 | Self-care portal | https://livquik.com/selfcare-portal-list/ This channel is open to Customers on a 24x7 basis. |

| 2 | support@livquik.comThis channel is open to Customers on a 24x7 basis. |

When submitting a complaint, customers are generally required to provide their essential details to ensure efficient processing. The information typically includes their identification, contact details, and a description of the issue. This may involve their name, a relevant account or reference number, address, phone number, email, and specifics regarding the nature of the complaint. Additionally, details related to any associated partners may be required to facilitate resolution.

The Customers will receive regular communication from the Company, during the Complaint resolution process, intimating the Customer at the following intervals:

- At the receipt of the Complaint;

- When an action is taken / at a decision-making step;

- Reasons for delay in actioning on the Complaint, if

- any; Follow-up action; and,

- Periodic updates regarding progress of complaint resolution.

The Company strives to resolve all escalated grievances at the earliest by assigning them the highest resolution priority. To make this a seamless process, Customers are advised to attach their ‘Customer reference number’ along with their escalation requests and in all communication with the Company. This allows the Company to resolve all grievances in a fast and efficient manner.

Escalation Matrix

The ensuing paragraphs outline in detail, the escalation matrix formulated by the Company for Customers to appeal and their respective TATs to ensure timebound resolution:

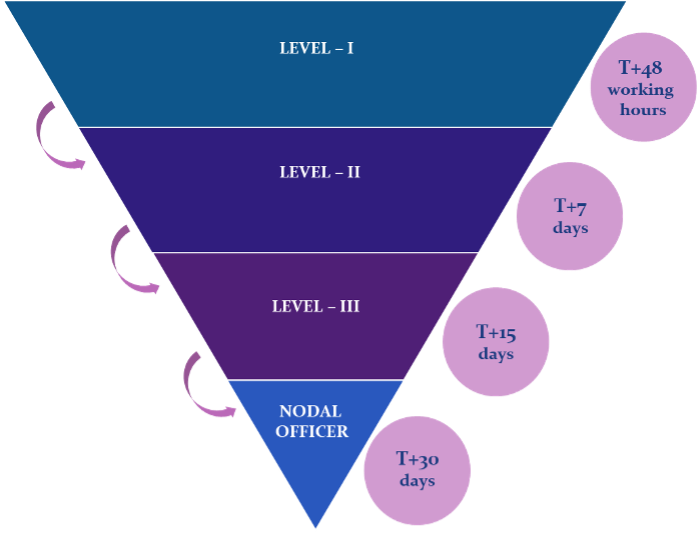

Level - I

This is the first level of processing all Complaints registered by the Customers via the three aforementioned channels. Once the Grievance is registered, a ‘customer reference number’ will be generated. The number will be attributed to that particular Complaint and can be used to track such Complaint.

This will be immediately followed by a Level - I Representative acknowledging the receipt of the Complaint and intimating the Customer with the details of the ‘customer reference number’. The day when the Representative acknowledges the receipt of Complaint will be known as ‘T’

The Level - I Representative will then endeavour to resolve the grievance within 48 business hours of acknowledging the Complaint, else the representative will intimate the Customer regarding the delay in complaint resolution.

Level - II

If the Complaint remains unresolved post the 48-hour timeline in Level - I, then it will automatically be escalated to Level - II. Additionally, if the Customer is not satisfied with the resolution provided by the representative or if the Customer does not get a response from the representatives within the defined timeline, then the Customer can escalate their Grievance to the Level - II. The Customer will attach their ‘Complaint reference number’ assigned to their grievance, to the escalation request in order to ensure speedy resolution.

Level - II Representative will endeavour to resolve the Complaints escalated to Level - II within T+7 days i.e., 7 (seven) days of the Complaint being registered at Level - I.

The contact details of the Level - II Representative are as under for Customers to escalate their complaints:

| Address | No.C-15, Sriram Nivas, Thiruvalluvar Nagar, Alandur, Kancheepuram, Chennai, Tamil Nadu - 600 016 |

| level2@livquik.com |

Level - III

If the Complaint remains unresolved post the T+7 days’ timeline, then it will automatically be escalated to Level - III on T+8th day. Additionally, if the Customer is not satisfied with the resolution provided by the Level - II Representative or if the Customer does not get a response within the defined timeline (T+7), then the Customer can escalate their Grievance to Level - III Representative at LivQuik. The Customer will attach their ‘Complaint reference number’ assigned to their grievance, to the escalation request in order to ensure speedy resolution

Level - III Representative will endeavour to resolve the Complaints escalated to Level - III within T+15 days i.e., 15 (fifteen) days of the Complaint being registered at Level - I.

The contact details of Level - III Representative are as under for Customers to escalate their complaints:

| Address | No.C-15, Sriram Nivas, Thiruvalluvar Nagar, Alandur, Kancheepuram, Chennai, Tamil Nadu - 600 016 |

| level3@livquik.com |

Nodal Officer

If the Complaint remains unresolved post the T+15 days’ timeline, then it will automatically be escalated to Nodal Officer on T+16th day. Additionally, if the Customer is not satisfied with the resolution provided by Level - III or if the Customer does not get a response within the defined timeline (T+15), then the Customer can escalate their Grievance to the Nodal Officer appointed by LivQuik. The Customer will attach their ‘Complaint reference number’ assigned to their grievance, to the escalation request in order to ensure speedy resolution.

Then Nodal Officer will endeavour to resolve the Complaints within T+30 days i.e., 30 (thirty) days of the Complaint being registered at Level - I.

The contact details of the Nodal Officer are as under for Customers to escalate their complaints:

| Name | Mr. Amiya Ranjan Sahoo |

| Address | No.C-15, Sriram Nivas, Thiruvalluvar Nagar, Alandur, Kancheepuram, Chennai, Tamil Nadu - 600 016 |

| nodalofficer@livquik.com | |

| Phone no. | (+91) 7845 811 694 |

RBI – Integrated Ombudsman

The Company strives to resolve all Grievances within a 30-day timeline from the receipt of the Complaint. However, in the unfortunate circumstance that a Complaint has not been resolved within the 30-day timeline or if a Customer is unsatisfied with the resolution provided by the Company after exhausting all escalation levels, they may appeal their grievance to the RBI Ombudsman (under the Reserve Bank – Integrated Ombudsman Scheme, 2021). The complainant can lodge their grievance on the ‘Complaint Management System’ (CMS) portal of the RBI by clicking on the link below:

https://cms.rbi.org.in/sn/app/login/login

In cases of loss/theft of card or fraud/abuse of wallet

The Company is committed to minimising financial crime and in particular to preventing, detecting, investigating and reporting fraud. LivQuik conducts its business with honesty and integrity and promotes ethical business practice across its organizational structure. LivQuik is fully committed to reducing the risk of fraud and its impact on the Company, its reputation, its customers, its employees and its stakeholders.

The Company shall endeavour to create sufficient awareness and educate customers in the secure use of the PPIs. This will include safekeeping of passwords, ensuring that pins remain confidential and the procedure to be in case of loss or theft of card or authentication data or if any fraud / abuse is detected, etc.

(Note: the procedure for such grievances is the same as outlined above)

Customer Compensation and TAT for failed transactions

In accordance with RBI’s “Harmonisation of Turn Around Time (TAT) and Customer compensation for failed transactions using authorised Payment Systems, 2019”, the Company has defined a Customer compensation and TAT process for failed LivQuik transactions.

The details of the process are as under:

(Note: Here, T is distinct from that defined in section (5.3.1). T refers to the day and calendar date of the transaction.)

| S.No | Product | Description | Timeline for auto-reversal | Compensation payable |

|---|---|---|---|---|

| 1 | Off-Us transaction | PPI transaction conducted using rails such as

| Basis the rules of respective payment system | |

| 2 | Automated Teller Machines | Customer’s account debited but cash not dispensed | Pro-active reversal of failed transaction within a maximum of T + 5 days | INR 100/- per day of delay beyond T + 5 days, to the credit of the account holder |

| 3 | Card Transaction | Card to card transfer Card account debited but the beneficiary card account not credited. | Transaction to be reversed latest within T + 1 day, if credit is not effected to the beneficiary account | INR 100/- per day of delay beyond T + 1 day |

| 4 | Card Transaction | Point of Sale (PoS) (Card Present) including Cash at PoS Account debited but confirmation not received at merchant location i.e., charge-slip not generated. OR Card Not Present (CNP) (e-commerce) Account debited but confirmation not received at merchant’s system. | Auto-reversal within T + 5 days | INR 100/- per day of delay beyond T + 5 days |

| 5 | IMPS | Account debited but the beneficiary account is not credited | If unable to credit to beneficiary account, auto reversal by the | INR 100/- per day if delay is beyond T + 1 day |

| 6 | UPI | Account debited but the beneficiary account is not credited (transfer of funds) | If unable to credit the beneficiary account, auto reversal by the Beneficiary bank latest on T + 1 day. | INR 100/- per day if delay is beyond T + 1 day |

| 7 | UPI | Account debited but transaction confirmation not received at merchant location (payment to merchant) | Auto-reversal within T + 5 days | INR 100/- per day if delay is beyond T + 5 days |

| 8 | On-Us transaction | PPI debited but transaction confirmation not received at merchant location OR Beneficiary PPI not credited. | Reversal affected in Remitter’s account within T+1 days. | INR 100/- per day if delay is beyond T + 1 days |

Reporting of unauthorised transactions and liability of the Customer

With the increasing thrust on financial inclusion and customer protection, the RBI vide its Notification titled ‘Customer Protection – Limiting Liability of Customers in Unauthorised Electronic Payment Transactions in Prepaid Payment Instruments (PPIs) issued by Authorised Non-banks’ dated January 4, 2019 issued guidelines outlining the liability of customers in cases of unauthorized transactions.

To ensure a safe and secure environment for conduct of transactions electronically, LivQuik has invested in technology with robust security systems and fraud detection and preventions mechanisms. The Company provides its Customers with 24x7 unauthorised transaction reporting facility which includes channels mentioned above in Grievance Redressal process. Further, all transaction and service-related calls will originate from the verified service number 1600118250 under the secure ‘1600xx’ series, ensuring trusted communication and customer security.

Further, to ensure accurate determination of a Customer’s liability, the Company’s communication systems used to send alerts and receive responses of Customers thereto, shall record time and date of delivery of the message and receipt of customer’s response, if any. On receipt of report of an unauthorised payment transaction from the customer, LivQuik will take immediate action to prevent further unauthorised payment transactions in the PPI. The ensuing paragraphs outline the Unauthorised transaction reporting process and details on customer’s liability against such transactions.

Channels of reporting unauthorized transactions

A Customer can report the incidence of an unauthorized transaction via email support@livquik.com toll-free helpline number - 1800 309 2225 or a direct link provided on the Company’s website and mobile app. The Customer can report an unauthorised transaction on a 24x7 basis across all channels.

The Customer will then receive a communication from the Company, acknowledging the receipt of the Complaint and providing the Customer with a complaint reference number.

Force Majeure

LivQuik shall not be liable to compensate customers for delayed credit if some unforeseen event (including but not limited to civil commotion, sabotage, lockout, strike or other labor disturbances, accident, fires, natural disasters or other “Acts of God”, war, damage to LivQuik facilities or of its agents, absence of the usual means of communication or all types of transportation, etc., beyond the control of LivQuik prevents it from performing its obligations within the specified service delivery parameters

Unauthorised transactions – Extent of Customer’s liability

A Customer’s liability based on the nature of an unauthorised transaction and the time taken by the customer. This is because the longer a Customer takes to report such transactions, higher is the risk of loss to the Customer or the Company. The following table represents the Customer’s liability:

| S.No | Particulars | Maximum Liability of Customer |

|---|---|---|

| (a) | Contributory fraud / negligence / deficiency on the part of LivQuik, irrespective of whether or not the transaction is reported by the customer. | Zero |

| (b) | Third party breach where the deficiency lies neither with LivQuik nor with the Customer but lies elsewhere in the system, and the Customer notifies the Company regarding the unauthorised payment transaction. The per transaction Customer liability in such cases will depend on the number of days lapsed between the receipt of transaction communication by the customer from the LivQuik and the reporting of unauthorised transaction by the Customer to the Company - | |

| I. Within three days# | Zero | |

| II. Within four to seven days# | Transaction value or INR 10,000/- per transaction, whichever is lower | |

| III. Beyond seven days# | 100% | |

| (c) | In cases where the loss is due to negligence by a Customer, such as where they have shared the payment credentials, the Customer will bear the entire loss until they report the unauthorised transaction to LivQuik. Any loss occurring after the reporting of the unauthorised transaction shall be borne by the Company. | |

| (d) | The Company may also, at its discretion, decide to waive off any Customer liability in case of unauthorised electronic payment transactions even in cases of Customer negligence. | |

| # The number of days mentioned above shall be counted excluding the date of receiving the communication from LivQuik. | ||

Reversal timeline for zero liability / limited liability of the Customer

LivQuik will strive to initiate a notional credit of the transaction amount into a shadow account within 10 days of receipt of such Complaint about unauthorized transaction, irrespective of settlement of insurance claim, if any.

Additionally, LivQuik will endeavour to resolve the Complaint within 90 days of receipt of the grievance and attempt to establish the liability of the Customer, if any. If LivQuik is not able to either resolve the grievance or establish any customer liability within 90 days of receipt of the Complaint, then LivQuik will compensate the Customer in accordance with the liability clause outlined in the section above.

Burden of Proof

The burden of proving customer liability in case of unauthorised electronic payment transactions will lie on LivQuik.

Maintenance of Records

In compliance with relevant regulations, the Company will maintain records pertaining to Complaints it has received. An indicative list of such data is as under:

- Mobile no. of the Customer;

- Nature of complaints received;

- Status of the Grievance;

- Time taken to resolve the Complaint, if resolved;

- Time taken for the Company to process Complaints at each escalation level, as applicable;

- Resolution provided; and

- Compensation awarded, if any.

Reporting and Monitoring mechanism

External reporting

LivQuik will strive to notify the RBI promptly of any breach in security or leakage of confidential information about its Customers. Additionally, Company will submit the PPI Customer Grievance Report to the RBI on a quarterly basis, as prescribed in Annexure 6 of the PPI Master Directions.

Internal reporting

LivQuik will report customer liability cases to the Board or to a relevant Committee of the Board.

The reporting will, inter-alia, include volume / number of cases and the aggregate value involved and distribution across various categories of such cases.

Monitoring mechanism

The Monitoring mechanism of the Company involves monitoring the grievances received by the Company periodically. Then the Customer Support team will analyse the parameters and provide their recommendations to improve and enhance the Customer Grievance process. These parameters will include:

- Complaints received and resolved beyond the prescribed TAT;

- Number of complaints escalated;

- Type of complaints escalated to Nodal officer / Digital Ombudsman; and

- Any deficiency in the manner the complaints are handled etc.

Review of the Policy

The Company will review the Policy at least once a year, or sooner, if it makes changes impacting the Company's business operations or due to changes in the regulatory framework. Any such policy changes will be approved by the Board and communicated to all relevant departments.

The Board or one of its Committees shall review on a quarterly basis, the unauthorised electronic payment transactions reported by customers or otherwise, as also the action taken thereon, the functioning of the grievance redressal mechanism and take appropriate measures to improve the systems and procedures.